The stablecoin wars appear to have began with a most interesting revelation coming out of the Proof of Keys test of Binance, which is still sort of on-going.

Austin Campbell, the Head of Portfolio Management at Paxos which does the actual issuing of bUSD on the ethereum blockchain, says and we’ll quote at some length:

“As a general statement, a properly designed fiat backed stablecoin should take customer money and put that money in safe reserves(1) in the traditional financial system. The problem is those reserves run on the rails of the traditional financial system. This means if you own treasuries, they settle T+1. If you have overnight reverse repo, that settles T+0. If you own money market funds, they settle T+2 (but often faster, thanks money managers). And all of those T mean business days, during banking hours (9–5pm, New York time), on days where banks are open (so not weekends and not holidays)…

Now what if someone wants to mint or burn a bunch of stablecoins at 3am NY time on Saturday?

Yeah. About that.

As a result, most stablecoin issuers (at least Paxos and Circle that I can personally confirm) keep money at US banks with fast payments networks. These are internal networks that can do 24/7 fast payments, using a private ledger or blockchain. Some of the luminaries in this space who can also bank crypto have historically included Silvergate and Signature.

However, you’d be a crazy person to keep ALL your deposits at a single bank, especially as they get large. You can’t keep $20B in uninsured deposits and be a stablecoin. Thus, all the stablecoins manage their liquidity and leave some millions to hundreds of millions to billions at these banks, and the rest of the reserves in tradfi instruments.

So let us say a stablecoin, we will call it CUSD for Canonical USD as our example, has $10B of assets. Maybe CUSD keeps $500mm at these fast payments banks, or 5% of total assets.

What that means is that CUSD can burn $500mm of the $10B during off hours, but if a $1B redemption comes in at our previous 3am Saturday NY time, you have to wait until NY banking hours to fulfill the remainder of it.

Is there an issue with the assets of CUSD? No. It’s just a timing issue. But this timing issue can break pegs temporarily and is consistently a source of stablecoin FUD because people do not understand how settlement works in traditional financial markets…

Part 2: Autoconversion

Binance engages in something called auto-conversion when there are deposits onto their platform. This means if a user deposits USDC, TUSD, or USDP to Binance, Binance will take those tokens, redeem them for fiat, and use that fiat to mint BUSD through Paxos.

So if Binance receives $1B in USDC deposits, how much USDC does Binance hold?

$0. They hold $1B BUSD instead.

The complication here is that Binance also allows users to withdraw back to other coins, so if Binance receives $1B of withdrawal requests for USDC, they need to do the following:

1 — Redeem BUSD against the BUSD trust

2 — Mint USDC with the proceeds from the BUSD redemption

3 — Sent the USDC to the user

This is a trivial thing to do during NY banking hours, but when you are off hours, as discussed above, things can break if the redemption activity is large.”

There’s a lot to unpack here. First of all, the poor – globally speaking – use cash, the actual paper. The middle uses bank money, insured by the state – the public – up to generally $250,000. The rich use government bonds or treasuries or reverse repos which are kind of the same thing. They do so because these bonds are ‘insured,’ as in the state has to pay them back up to any amount, including billions.

These bonds are traded as you trade bitcoin, though in slower and older systems, and therefore you have a hot and cold wallet system here too where you keep some in ‘cash’ at the bank and most ‘invested’ in bonds.

That suggests Binance temporarily paused withdrawals of USDc on Tuesday because the ‘hot’ fiat wallet was depleted, in addition to the portion of USDc they hold in USDc. They had to tap into bonds, and those are not instant transfers, so everyone had to wait until banking open hours.

The attack vector here is stated by Campbell himself. You wait until 5PM New York time, preferably during a long weekend, attack the peg knowing it will come off peg, that adds credibility to your FUD, trap some of the crowd and then release.

This dump and pump has occurred many times on Tether. We assume organically as they did actually have banking problems some years ago, with the peg restored once those banking issues were resolved.

Here however we have another layer of complexity because we’re not dealing with 1:1, but with 1:1:1.

We can ignore the last one, which is USD, focus instead only on the peg between bUSD and USDc, and we can easily imagine what some people might imagine they can do.

You can move the peg up as well of course, the other down, and a lot of combinations as well as maths, all of which is none of our business.

So, why add this extra complexity? In addition this naturally also raises another question: is it actually limited to just USDc?

bUSD Dominates Binance

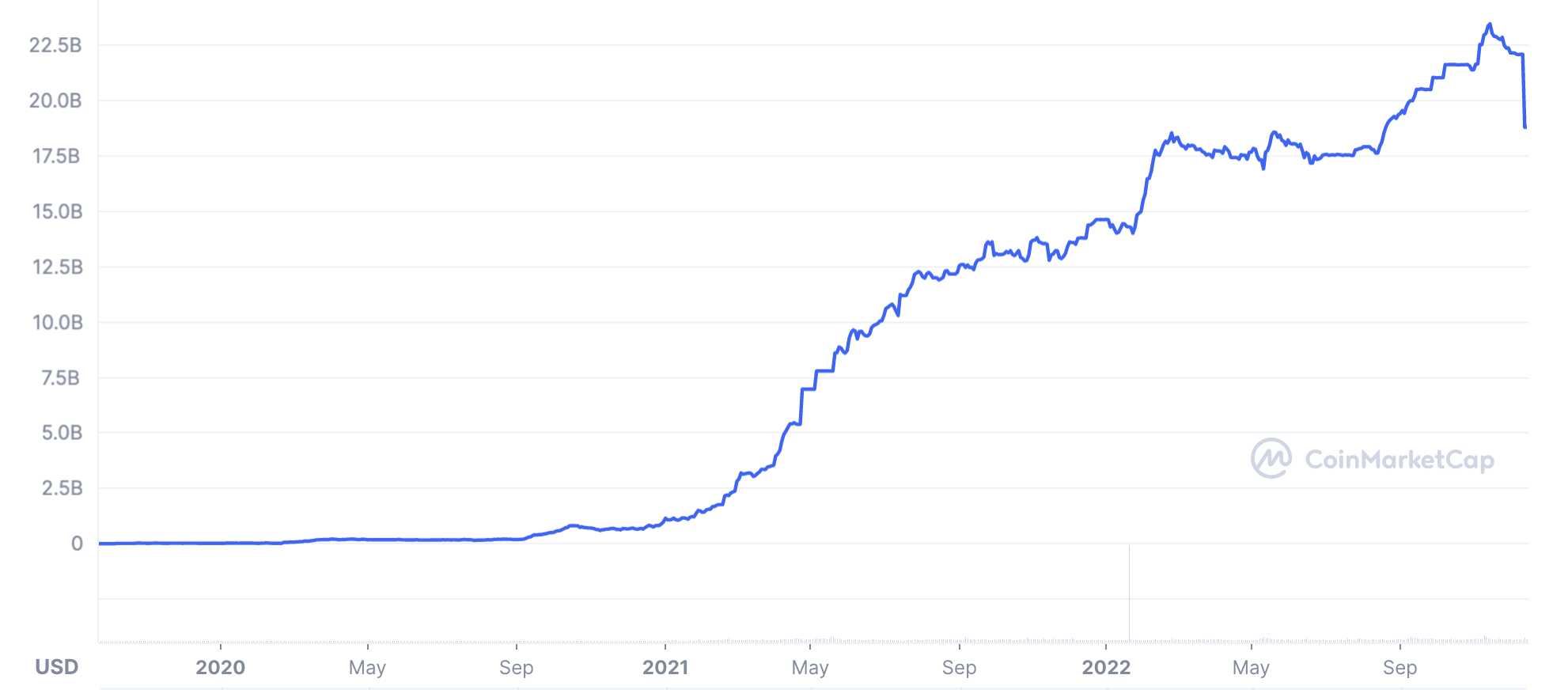

bUSD, a stablecoin issued by Binance itself, is the top holding on this exchange, amounting to 25% of all assets.

They have $15.4 billion bUSD according to revealed on-chain wallets, and curiously enough that amounts to almost the entire market cap of bUSD at $18.8 billion.

Those may be just interesting numbers with Tether being their second biggest holding, showing they’re clearly not bUSD-ing Tether.

They do actually have about $3 billion of USDc, although whether that is new deposits that have not yet been converted is not too clear.

As bUSD is their own stable, one can perhaps understand why they’d bUSD the deposited USDc, not least because that’s potentially one way to increase the market cap of bUSD.

The bUSD, as can be seen, has been growing very fast in about two years, seeing a sharp fall recently in light of the on-going mass withdrawals.

The token provides lower fees on Binance for holders, so it has some utility, and therefore its concentration on Binance might not be too surprising, but the USDc conversion is if not surprising, then new information.

The only way we can think it of making sense is that they can’t do anything with USDc, without us all seeing it, but converting that USDc into fiat and minting a new bUSD for that fiat can allow them to earn yields on treasuries and so make money.

But, why not tether as well, or dare we say bitcoin. With the latter it would be dangerous because it is volatile. It can go down for sure, but it can also go very up and you won’t be able to buy it and you go bankrupt.

With Tether, as it is meant to be stable, that sort of risk wouldn’t apply, but there can be other potential risks.

If Tether goes bankrupt for example, you still have to buy all the USDt to give it to your customers to withdraw if they want.

You’d be buying them at a discount, but if you’re buying billions, in this case $12 billion, and from the open market since Tether is no more, the peg might moon instead of crash and you get in a bitcoin like situation, potentially.

So one can speculate they don’t do Tether due to not having as sufficient trust as in USDc, just as one can speculate the more obvious that Bitfinex is sort of irrelevant, while Coinbase is actually the biggest exchange by asset holdings and thus more their competitor.

By doing what they do, they both lower USDc’s market cap while increasing theirs, or at least assist towards it, while keeping tether at the top.

Someone at Coinbase would probably see it as some sort of attack. Others would say it’s just business, but what we are more concerned with is whether it is safe.

The Web of un/Stables

Stablecoins peaked at a combined market cap of about $150 billion and even at the depth of this bear still stand at $120 billion.

“Are runs on stablecoins going to cause massive contagion that crashes the financial system No. Also stop,” says Campbell.

Well, at this size maybe they still are small, but if cryptos 10x and stables reach $1 trillion, you would be getting in the territory of unknown unknowns in the traditional system.

As it would hurt them far far more than crypto, and crypto might actually boom as everyone would run from stables to crypto, arguably we can discount another potential attack vector in this bUSD-ing where banks in concert implement a blockade for longer than just a long weekend.

We can discount it because they risk hurting themself not just far more, but potentially fatally as the bitcoin blockchain of course wouldn’t be affected by any of it in as far as the blocks would keep moving, while whether banks would keep processing transactions in a potential calamity of the 10x the size of current stablecoins, is to be thought.

This web of stables however can affect crypto in a different way in as far as two of the biggest crypto exchanges, and three if we include Bitfinex, are tied to their own stable.

With this bUSD-ing of USDc, bUSD and USDc are also arguably tied together, especially at bigger scales, and thus if something goes fatally wrong, two of the biggest exchanges can in theory vanish.

That extreme is difficult to see, but that this bUSD-ing of USDc will probably be played somehow, is not because we have friction in the banking system and here a fairly complex setup.

Safe Cryptos, Shenanighaning Stables?

We could describe, out of desire more than fact, a (current?) state where everyone has learned the lesson that you can’t play with crypto because it is volatile. Gox made that clear.

But stables are new still, they have their own quirks in as far as you’re ‘scanning’ the effectively paper fiat system, and so it has its own demands like needing to have bonds if you’re going to get anywhere near the equivalent of holding crypto in sums above $250,000.

This system has not been tested, even though it has been running for some time, and we assume it will go fractional reserve at some point because banking did, so why wouldn’t this as it requires the same level of unverifiable trust.

With rising interest rates in addition it might be quite tempting to get that yield, and so this run on Binance was sparked by an audit which was limited to only bitcoin.

What about eth, or other cryptos? We’d doubt they’d play with those in bUSD-ing them because that of course would be very dangerous, but they need to clarify why they are bUSD-ing USDc and are they doing the same to any other asset.

There is a Proof of Keys on-going on Binance, so if there was anything else presumably it would have or will come out, with no other withdrawal problems reported so far.

Yet this method of issuing your own token, keeping the other in ‘cash,’ links them all together so if there’s trouble in one, potentially they all fall.

That’s not something we’d necessarily call shenanigans, but it adds another layer of risk to centralized crypto exchanges which in practice translates to don’t send USDc to Binance as you might just increase that risk.

Without more clarity, including risk assessments, some might even go as far as say don’t use Binance at all, and now they definitely need a full on audit of all their assets so that we can see just what else is not quite 1:1, if anything.

In theory since they are linked, though the amount is small, one can also at the extreme say don’t use Coinbase either.

As a matter of principle in fact saying so is easy because we don’t want a concentration of exchanges. Arguably both Binance and Coinbase are too big, considering the amount of assets they hold. Certainly Coinbase.

Decentralization of centralized exchanges has its own problems however as they need the highest level of security first of all, and of course they need to gather sufficient trust that they won’t shenanigans.

That’s a high bar, but the best way to minimize risk is to diversify it and having more good exchanges would be a direct way of minimizing the risk of too big to fail crypto exchanges.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.